Secondhand activity narrowed toward the handysize and small tanker segments through the week, while owners kept signing tanker and gas newbuilding contracts at pace and recyclers competed for a thin supply of candidates.

Crude sale and purchase was quiet at the top of the size range, with one large unit changing hands. A 297,000 dwt VLCC built 2011, scrubber fitted, sold to Korean buyers at USD 82 million for delivery in the first quarter of 2027. The transaction sets a clear reference for early-2010s tonnage carrying exhaust gas cleaning systems and forward delivery terms.

Activity was heavier at the small end. A pair of stainless steel chemical tankers of about 20,000 dwt, built 2006 and 2008, sold together for around USD 23 million with time charters attached, the income stream supporting the price. A 17,000 dwt unit from 2008 fetched USD 9 million, and a 14,000 dwt 2010-built coated tanker went to Vietnamese buyers at USD 10.5 million. Buyers at this size continue to favour vessels that arrive with employment in place.

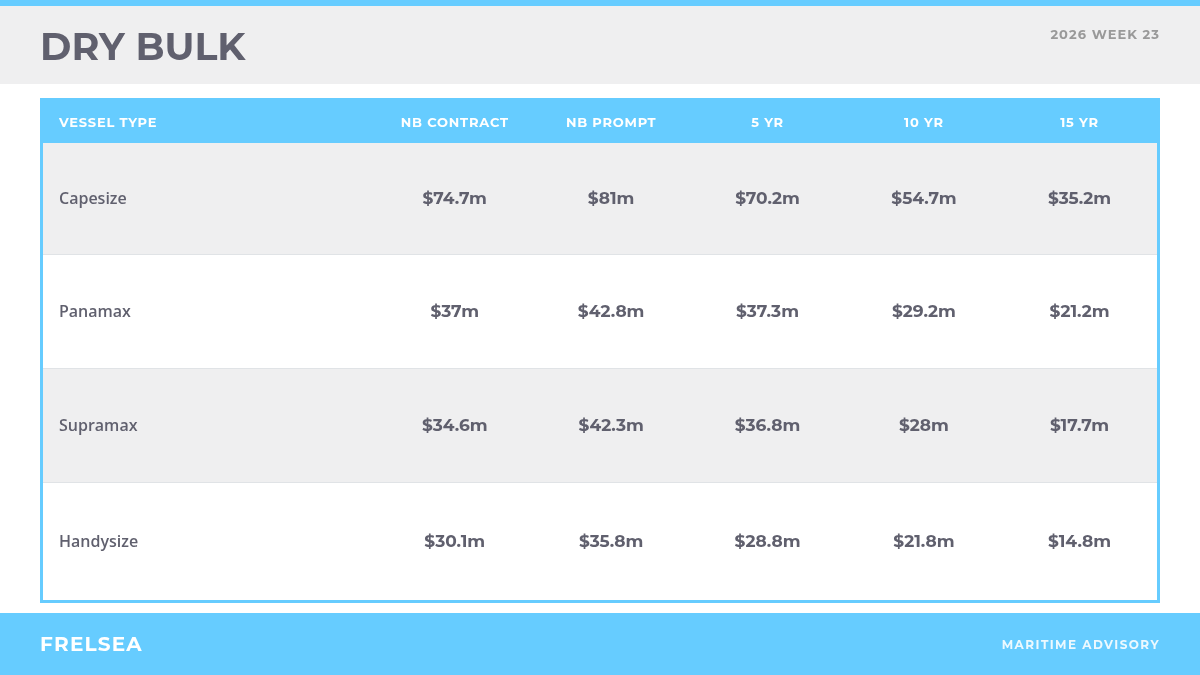

The newbuilding side was where tanker money concentrated. A Greek owner signed for twelve 307,000 dwt VLCCs at a Chinese yard at about USD 123 million each, the first crude carriers of that size contracted at the facility and a single order worth close to USD 1.5 billion. Further VLCC pairs, Suezmaxes around 158,000 dwt at roughly USD 84 million, and Aframaxes near 114,000 dwt at about USD 73 million were booked across Chinese and Korean yards. Smaller product orders ran from LR1 units at USD 62 million down to MR carriers between USD 45 and USD 54 million depending on yard and specification. The volume signals continued confidence in tanker earnings well into the end of the decade.

Capesize secondhand business returned with an older pair. Two Japanese-built units from 2001 and 2003 sold en bloc to Chinese buyers for USD 31 million combined, a level that anchors pricing for early-2000s tonnage facing near-term special surveys.

Kamsarmax interest spanned the age curve. A 2024-built resale changed hands at USD 42.7 million, while a 2008 unit sold for USD 14.85 million, the spread reflecting how sharply the market separates modern eco tonnage from older ships. Supramax sales were value-driven, with a 2006 vessel sold through an online auction at USD 9.05 million, a 2002 unit at USD 8.5 million, and a 2004 ship at USD 10 million.

Handysize was the most active dry segment. A pair of 2017-built open hatch box-shaped units sold for USD 22 million each, setting the upper marker for the size. A 2013 vessel followed at USD 17.7 million and another at USD 17 million. Older tonnage filled out the list, with three units built between 2010 and 2011 trading between USD 10.5 and USD 10.8 million, several carrying attached charters or ice class. Demand for geared handies remains broad across buyer nationalities.

Dry newbuilding ordering continued alongside. A Greek owner booked two 180,000 dwt capesizes at about USD 78 million each, and a Newcastlemax pair near 211,000 dwt was contracted at USD 77.5 million. Ultramax orders in the 64,000 to 65,000 dwt range clustered between USD 34 and USD 35 million at Chinese yards, with further units placed in Japan.

Recycling markets traded firm but starved of tonnage. The week followed the Eid holidays and ran into the approaching monsoon, both of which thinned the flow of vessels to the beaches even as yards across the subcontinent kept competing for any genuine candidate.

A handful of sales cleared. An LNG carrier of about 33,000 light tons went to India, a 2001-built bulk carrier was sold to Turkey, and a small container vessel went to Bangladesh, alongside a general cargo unit and a reefer also committed to Bangladesh. The bias toward smaller and specialist units reflected the scarcity of large candidates rather than any softening in appetite.

Pricing held across the basin. Bangladesh and Pakistan retained the firmest levels, with India close behind as a recovering Rupee eased import costs for local mills. Steel plate prices softened modestly in India and Bangladesh and held flat in Pakistan, keeping recyclers price-sensitive on offered levels. Turkey stayed well below the subcontinent across all vessel types, its relevance concentrated in European-regulated and specialist work. With freight earnings firm and the geopolitical backdrop easing, owners have little reason to release tonnage, and the supply-short pattern looks set to run through the rest of June.