The secondhand and demolition markets were active in Week 22, with a high volume of dry bulk sales offsetting a softer tanker freight backdrop and quiet recycling yards amid Eid holidays.

Freight markets corrected across most tanker segments this week as the Strait of Hormuz remained closed to commercial transit, leaving Arabian Gulf volumes depressed and owners cautious about vessel deployment. VLCC activity in both the Arabian Gulf and West Africa was thin, with charterers well-supplied and owners unwilling to commit until the geopolitical outlook clarified. Atlantic Suezmax rates fell sharply: Nigerian/UKC levels dropped below WS 150 as over 20 prompt ships queued near Bonny, while CPC recorded WS 225 last done on TD6. The Aframax market was divided — the Mediterranean recovered mid-week as prompt tonnage cleared, with TD19 firming to WS 180 by Friday, while the North Sea corrected to WS 145 after charterers drew double-digit offers for a single cargo. LR2 and LR1 markets continued to deteriorate, with laden vessels trapped inside the Gulf and rates falling at each fixture. On the product side, UKC MR rates declined further, with TC2 trading around WS 155 and TC14 falling to WS 140 before rebounding to WS 235 by the close — a recovery that could redirect ballasters away from Northern Europe.

Against this soft freight backdrop, secondhand activity was notable. Scorpio Tankers sold four 2014/2015-built LR2s — STI BROADWAY, STI CONDOTTI, STI WINNIE, and STI LAUREN — in a single en bloc transaction for a reported USD 258.8 million, approximately USD 64.7 million per vessel. The 2002-built VLCC ABIE changed hands at around USD 41.5 million, a useful benchmark for vintage crude tonnage. HELLAS FIGHTER, a 2015-built HMD MR, was placed with a Greek buyer at USD 39.25 million. HANS MAERSK (MR1, 2009, STX) sold at USD 21 million, and OKEE JOHN T (MR2, 2006) cleared at around USD 16 million.

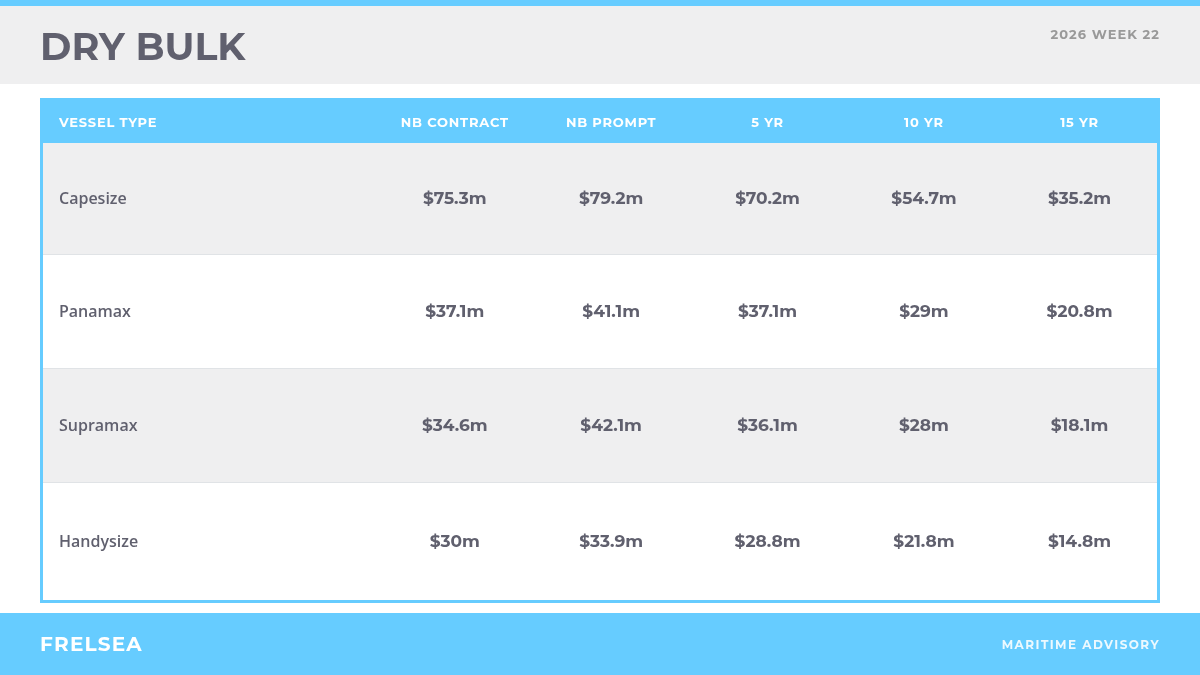

The dry bulk freight market strengthened through the week. The Baltic Capesize Index rose to a two-week peak of 5,503 points by Friday, with Pacific round voyage rates reaching USD 52,950 and Atlantic transatlantic earnings climbing to USD 55,275 on limited prompt availability. The Panamax index advanced 5.4% week on week to 2,343 points, supported by steady Australian mineral demand and Indonesian coal flows pushing Pacific round voyage rates to USD 23,350. Supramax traded in a flat range as fertiliser and minor bulk demand in the Atlantic offset broader weakness, while Handysize remained stable but range-bound.

The secondhand market saw one of its most active weeks of the year. EHIME QUEEN, a 2016-built scrubber-fitted Capesize from Nissen Kaiun, sold to Chinese interests at USD 57.5 million basis July–September delivery. Two sister SWS-built Capesizes, MARAN HAPPINESS (2008) and MARAN ARGONAUT (2009), sold en bloc for USD 60 million. At the Ultramax level, TIAN MU SHAN and YAN DANG SHAN, both 63,000 dwt 2017-built Sainty vessels owned by Zhejiang Shipping Group, were sold via online auction for USD 52.32 million en bloc. BELTIGER, a 2017 New Times Ultramax from Belships, was committed at USD 26.8 million. ASAHI OCEAN, a 2013-built Hakodate Handysize, was sold to a Vietnamese buyer at USD 15.25 million — flagged by brokers as a new benchmark for the type. The week also produced multiple en bloc disposals of older and mid-size tonnage across the Panamax and Supramax categories, keeping total volume unusually high.

Recycling yards across the Indian subcontinent operated at a subdued pace as Eid al-Adha holidays constrained activity in Bangladesh and Pakistan, while India attracted some underlying interest supported by a firmer rupee and rising domestic steel plate prices (INR 38,500–39,200 per tonne). Pakistan’s Gadani yards came to a near standstill and Turkish yards mirrored the regional quiet, with cautious economic sentiment persisting in Aliaga.

Indicative consensus rates for bulk carriers: India around USD 414/LDT, Bangladesh around USD 458/LDT, Pakistan around USD 442/LDT, Turkey around USD 280/LDT. Tanker rates held slightly higher across the board: India around USD 428/LDT, Bangladesh around USD 475/LDT, Pakistan around USD 457/LDT, Turkey around USD 286/LDT. Reported transactions were limited. GROUSE ARROW, a 1991-built open-hatch general cargo vessel of 42,276 dwt and 11,050 LDT, was committed to Indian buyers at USD 450/LDT. ON VICTOR, a 1997-built tanker of 8,320 LDT, was delivered to Alang at USD 375/LDT. In a regulatory development, the US Office of Foreign Assets Control granted cash buyer GMS specific licenses to acquire and recycle four sanctioned container vessels after a seven-month compliance review, though the vessels remain on the active OFAC list and face banking gridlock that limits practical beaching.