S&P activity ran heavy across both wet and dry markets, with modern resale tonnage finding ready buyers and Norden absorbing four 2024-built JNS Handymax resales en bloc.

Tanker S&P was firm despite continued moderation in freight earnings from the March peaks. The Baltic VLCC TCE closed the week around USD 220,361/day, down from late-April highs but still extraordinary by historic standards.

Two scrubber-fitted sister VLCCs, “C. Innovator” 314k/2012 Dalian and “C. Progress” 314k/2012 Hyundai, were committed en bloc at USD 120.6M including time charters into 2027 and 2028. A resale VLCC at Hengli, 306k/2026 prompt ex-yard, went to Trafigura at USD 163M. On the Suezmax sector, two scrubber-fitted Daehan 5111/5118 resales at 158k/2027 changed hands en bloc at USD 190M to Teekay. CMB.Tech sold “Stella” 165k/2011 Hyundai Samho at USD 67M basis SS/DD freshly passed, and the older “Aegean Horizon” 159k/2007 Hyundai found a buyer at USD 50.1M.

In the clean trade, the scrubber-fitted LR2 “STI Condotti” 110k/2014 Hyundai Samho was reported sold in excess of USD 70M, with TC1 closing the week around USD 147,560/day. On MR2s, “High Tide” 52k/2012 Hyundai Mipo went to Nusantara Maritime at USD 28.45M. Turkish buyers acquired the ice-class “Royal Jasmine” 53k/2008 Guangzhou for USD 20.7M, and TORM took two Zhoushan Changhong MR resales, “Horizon Andros” 50k/2027 and “Horizon Syros” 50k/2026, en bloc at USD 102M with scrubbers fitted.

Newbuilding activity was led by Pan Ocean booking four 320k VLCCs at Hanwha Ocean at USD 131M each for 2030. Ibaizabal Tankers of Spain ordered two 158k crude tankers at Hengli at USD 85M each for 2028, and Shishi Dingsheng placed two 114k Aframax crude tankers at Taizhou Kouan at USD 70M each for June 2029. The EU’s 20th sanctions package introduced new restrictions on tanker sales to third countries, requiring mandatory contractual clauses prohibiting resale to Russia and pass-through obligations on subsequent buyers, narrowing the pool of compliant buyers for older EU-flagged tonnage.

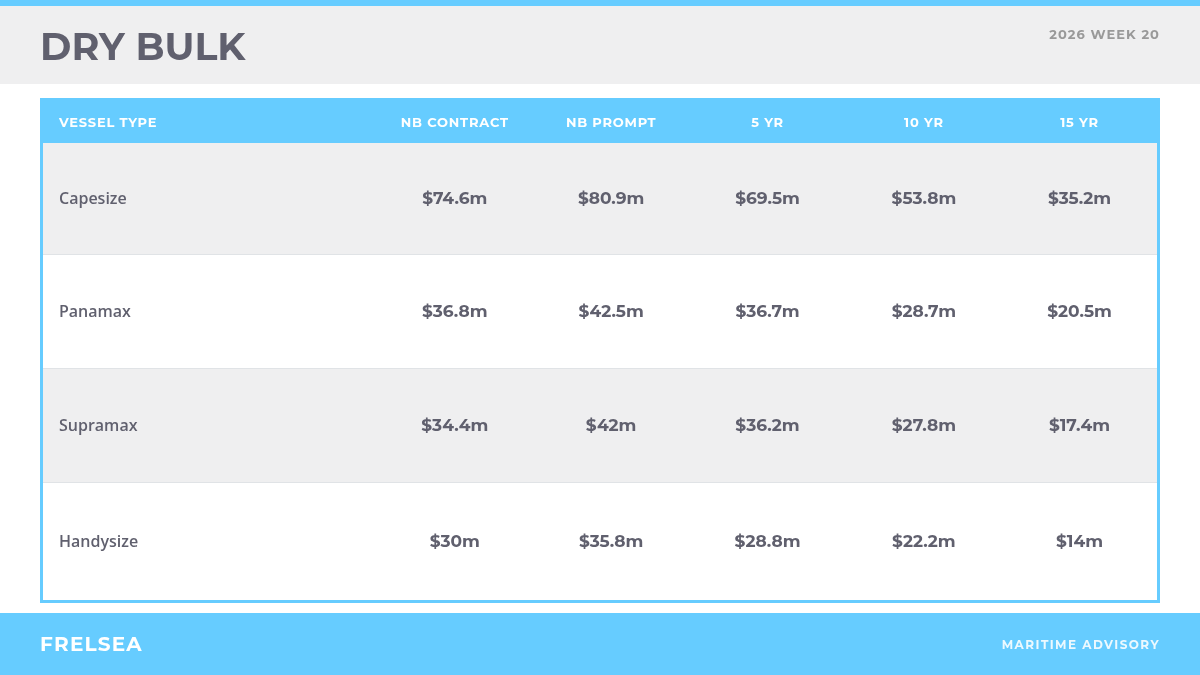

The Baltic Dry Index closed the week at 3,151 points, up 5.81% week-on-week, with all sub-indices firmer. Capesize trans-Atlantic earnings pushed above USD 55,000/day and the Kamsarmax 5TC closed at USD 22,691/day, up USD 2,592/day on the week. The strength translated directly into S&P appetite across Kamsarmax, Ultramax, Supramax and Handysize segments.

On the Capesize sector, “Pigassos” 176k/2011 SWS sold to Chinese buyers at USD 31.7M with SS/DD due, and the older “Chin Shan” 176k/2004 CSBC traded at USD 20.3M. Post-Panamax “Yangze 902” 93k/2012 Jiangsu went at USD 13M with a TC running to end-2026.

Kamsarmax activity was particularly heavy. Resale “Moana” 82k/2026 Yizheng Yangzi traded at USD 36.5M, “Joy” 81k/2019 Chengxi achieved USD 31M, and “Nord Polaris” 82k Tsuneishi Cebu was committed to Blumenthal at USD 28.25M. Older 2010/2011-built Kamsarmaxes traded in the high USD 17M region, with “HC Pioneer” 83k/2010 Sanoyas at USD 17.7M and “Avalon” 82k/2011 Sungdong at USD 17.5M to Chinese interests.

In the Ultramax segment, sister ECO units “Huayang Rose” and “Huayang Lily” 64k/2016 CSI were sold en bloc to Chinese buyers at USD 50.4M. Drydel’s “Dominator” 64k/2021 Shin Kasado went to Greek buyer Astrobulk at USD 38M, and Jinhui’s “Jin Chao” 64k/2014 Jiangsu Hantong was committed at USD 25.1M.

The Supramax sector saw OHBS “Sumaq Queen” 51k/2017 Imabari go to Greek buyers at USD 25M. Older 2008–2009 vintage Supramaxes cleared at firm levels, with “Messinian Spire” at USD 14.5M and scrubber-fitted “Xing Ning He” at USD 11M. Headline of the week was Norden’s en bloc acquisition of four 40k/2024 JNS Handymax resales at USD 121M, or USD 30.25M apiece. Newbuilding orders were measured: Eurobulk contracted two 82k Kamsarmaxes at Hengli at USD 37M each, and Safe Bulkers ordered one 182k Newcastlemax at Namura at USD 78.5M plus three 82k Kamsarmaxes at Japanese yards at USD 41M each, all for 2029.

Recycling activity in the Indian Subcontinent was limited, with sentiment subdued throughout. The Indian rupee slid to a new historic low near 96 against the US dollar, intensifying pressure on local buyers and reducing import competitiveness. Indian breakers narrowed workable levels for bulker tonnage to around USD 415/ldt, with steel demand softening alongside slower construction activity.

Bangladesh remained steady, though actual sales were constrained by heavy rainfall ahead of the monsoon and inventory backlogs at several yards. Chattogram bulker offers held around USD 460/ldt and tanker offers between USD 470 and USD 480/ldt. Pakistan’s Gadani market was more resilient, with the local rupee holding well against the dollar; tanker rates were quoted at USD 440/ldt and bulker rates at USD 460/ldt. Turkey remained constrained by lira depreciation and weak rebar demand, with Aliaga deep-sea levels around USD 280/ldt for bulkers and USD 310/ldt for tankers. Reported sales included the zinc-coated MR tanker “Maymei” 45k/1997 (9,728 ldt) to Bangladesh at USD 510/ldt, and the LPG carrier “Gas Crusader” 2k/1996 (1,481 ldt) to Bangladesh at USD 550/ldt.