The shipping markets experienced extraordinary volatility in Week 09, with crude tanker values reaching levels unseen since 2020 and dry bulk activity demonstrating broad strength across all vessel sizes. Geopolitical tensions, structural supply constraints and the migration of restricted tonnage back into mainstream markets created a perfect storm driving both freight rates and asset values to multi-year peaks.

VLCC sentiment reached fever pitch this week as markets repriced effective supply following renewed Middle East escalation. Benchmark TD3C earnings surged from WS163 to WS217 by week’s end, with rates pushing beyond WS225 on select fixtures late Friday. The spike reflects far more than seasonal strength. Effective compliant tonnage remains significantly constrained, with approximately 15% of VLCC and Suezmax capacity now operating in restricted or shadow fleets. Crude diversification flows, particularly India’s pivot away from Russian barrels and Venezuela’s return to mainstream trade after years of shadow-fleet dependency, have added structural demand without requiring global volume expansion. These factors, combined with geopolitical uncertainty around potential Strait of Hormuz disruption, created a risk premium on every fixture.

Suezmax markets erupted in parallel, with TD20 firming from WS164 to WS211–220 as VLCC strength naturally spilled into smaller crude carriers. CPC rates climbed even more dramatically, from WS200 into the WS230s as Black Sea tonnage supply tightened further. The Atlantic basin saw similar momentum, with AG/East and Basrah-westbound routes commanding historic premiums. On the secondhand front, VLCC asset values climbed sharply. A 300,000 DWT 2006 vessel achieved USD 51–52 million, while modern tonnage continued to command premiums reflective of the underlying market tightness.

Aframax and product markets added support across crude and refined trades. Med Aframax activity fluctuated through the week as weather improved and tonnage lists expanded, but ultimately stabilized around WS230 by Friday. AG LR2s posted their strongest week in 18 months, with TC1 climbing 35 WS points to WS220 as Asian-loading markets benefited from decreased ballaster supply and sustained charterer demand. LR1 rates similarly climbed WS215 on eastbound routes, supported by firming naphtha business and geopolitical premiums. MR2 secondhand values held firm at USD 44 million for modern 2020-built units, reflecting sustained confidence in shorter-cycle crude and product employment.

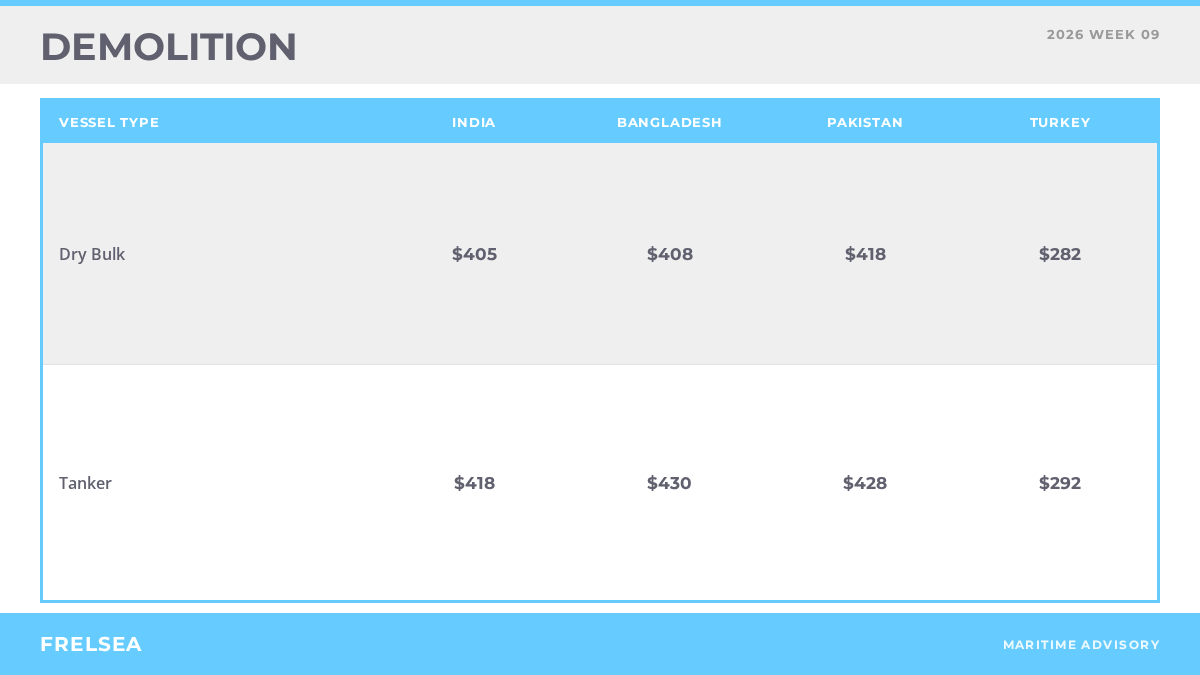

Demolition markets remained stable across South Asian yards, with tanker scrap prices holding steady at approximately USD 410–430 per LDT in India and Bangladesh. Turkish yards traded around USD 280/LDT. Limited activity during the week reflected ongoing preference for operational employment at elevated freight rates, with owners reluctant to exit vessels in a firm market environment.

Capesize markets traded sideways this week despite broad sentiment remaining positive. C5TC averages closed Friday at USD 24,211/day, down marginally from earlier sessions. Iron ore rates on the West Australia to China route maintained firmness at high 9.00s Worldscale, while longer-haul transatlantic and transpacific round voyages showed modest softening. Secondhand values for modern 2006-era capesize tonnage held around USD 26 million resale, with older units trading significantly lower.

Kamsarmax/Panamax activity picked up noticeably, with P5TC averages closing the week at USD 17,481/day, up USD 938 from opening levels. Trip routes from Skaw-Gibraltar to Far East improved modestly to USD 22,807/day, while Pacific round voyages gained USD 1,600/day to USD 19,729/day. Forward employment opportunities for summer delivery were actively discussed, with owners seeking to lock in favorable rates ahead of potential seasonal softening. Secondhand values for newer Kamsarmax tonnage (81,000 DWT 2014-built) reached USD 26.8 million on electronic main engine vessels, while older 2008 units traded around USD 13.6 million.

Ultramax and Supramax activity demonstrated the strongest momentum, with S11TC closing the week up USD 2,300/day at USD 16,915/day and S10TC gaining similar magnitude. Asian routes particularly outperformed, with China-to-Australia and Pacific round voyages firming 4–5,000 USD/day. Handysize markets provided further uplift, with H7TC closing at USD 13,976/day, up USD 1,200 from week’s opening. North China-Australia routes cleared USD 17,063/day, while regional East-West Asian employment remained strong at USD 10,819/day.

Secondhand values across all dry sizes showed consistent firmness. Modern Kamsarmax tonnage achieved USD 26.8 million, while Ultramax 63,000 DWT 2014-built vessels commanded USD 23 million. Supramax 55,000 DWT units of similar age traded around USD 14.5 million. Handysize secondhand markets reflected solid demand, with 40,000 DWT 2015-built tonnage achieving USD 19.5 million and 34,000 DWT units commanding USD 18.5 million.

Dry demolition prices remained unchanged from previous week, with Indian yards pricing around USD 390–410 per LDT, Bangladesh at USD 410/LDT, Pakistan at USD 410/LDT, and Turkish facilities at USD 270/LDT. Limited scrap activity during the week reflected owner preference for continued operation given supportive freight levels.

Demolition markets across both tanker and bulk segments demonstrated stability with minimal activity. Indicative South Asian pricing held firm at approximately USD 410/LDT in Bangladesh and Pakistan for both asset classes, with Indian yards slightly lower at USD 390–410/LDT. Turkish yards remained well below regional competition at USD 270–280/LDT. The week saw minimal deal flow, suggesting owner conviction in sustained higher employment levels continues to defer scrap recycling decisions.

Word count: 821