Tanker secondhand values moved sharply higher in Week 10 as buyer demand across all wet segments intensified, while dry bulk transaction volumes remained substantial across every size category and demolition pricing held steady in South Asian yards.

Tanker S&P activity in Week 10 was high across all size segments, with pricing reflecting firm demand for modern, compliant tonnage. In the Very Large Crude Carrier sector, a 308,930 dwt, 2005-built Samsung vessel with scrubber fitted committed at USD 38 million, while a 300,866 dwt, 2006-built IHI unit was sold at USD 51.5 million, the premium over the older Samsung unit illustrating the value buyers continued to place on build year and yard pedigree.

The Suezmax segment recorded particularly strong pricing. A 159,039 dwt, 2013-built Samsung vessel with scrubber fitted committed at USD 63 million. A 156,092 dwt, 2013-built Sumitomo unit with scrubber fitted, with drydock falling due in June 2026, was acquired by Greek interests at USD 65 million. Both transactions represented a material step up from prior weeks and confirmed sustained demand for modern Suezmax tonnage.

Aframax trading was extensive. A 2018-built Chinese-built unit of 112,532 dwt with scrubber fitted achieved USD 71 million, setting a strong reference point for the size. Two 2008-built Tsuneishi units committed at USD 33.5 million and USD 33 million respectively, and a 2009-built Samsung Aframax with scrubber fitted was sold at USD 41 million. In the LR2 segment, a 2015-built Sungdong unit of 109,999 dwt with scrubber fitted committed at USD 60 million, following its sister vessel’s sale in January at USD 57.5 million, while a 2009-built Sungdong LR2 also with scrubber fitted achieved USD 41 million. A 2006-built LR1 of 72,782 dwt built at Dalian committed at USD 12.5 million.

Medium Range tanker activity was also active. A 2020-built Hyundai Mipo pair of 50,185 dwt each with scrubbers committed en bloc at USD 45.25 million per unit. A 2017-built Dae Sun unit of 50,583 dwt achieved USD 38 million, and two 2015-built Hyundai Mipo sisterships of 49,990 dwt each with scrubbers were committed at USD 35 million per vessel. An older 2008-built Hyundai Mipo unit achieved USD 17.75 million, and a 2005-built Korean-built MR sold to Nigerian interests at USD 12 million. Additionally, two 2010 and 2009-built Hyundai Mipo MR2 sisterships with scrubbers and ML coating were committed en bloc at USD 48 million combined.

On the newbuilding front, Performance Shipping ordered two Suezmax vessels of 158,000 dwt at USD 81.5 million each, one at SWS for 2029 delivery and one at CSTC for 2028 delivery, both to be fitted with scrubbers.

Dry bulk S&P activity in Week 10 was broad-based, with buyers from China, Greece, India, Turkey, and elsewhere active across all major size segments. Two Capesize transactions were reported: a 177,947 dwt, 2007-built SWS vessel committed at high USD 23 million, and a 175,607 dwt, 2011-built HHIC Philippines unit with scrubber fitted committed at excess USD 32 million. A spread of this magnitude between the two units reflects both the scrubber premium and the age differential.

Kamsarmax trading was active. A 2020-built scrubber-fitted Jiangsu unit of 81,795 dwt achieved approximately USD 32 million, while a 2014-built JMU Japan unit of 81,094 dwt was acquired by Great Eastern Shipping of India at excess USD 27 million. A 2011-built Tsuneishi Kamsarmax changed hands at USD 19.35 million, a 2008-built Mitsui Japan unit sold to Chinese interests at USD 13.6 million, and a 2010-built New Century China unit committed at USD 11.7 million. Three Post-Panamax vessels of approximately 93,000 dwt built in 2010 and 2011 at Jiangsu committed in the USD 11.6 to 11.8 million range.

Ultramax transactions included a 2026-built resale of 63,800 dwt at Nantong acquired by Greek interests at USD 36.5 million, a 2016-built Imabari unit of 63,503 dwt at excess USD 28 million, and a 2014-built Jiangsu unit of 63,800 dwt at USD 23.4 million. In the Supramax segment, two 2005-built NACKS sisterships of approximately 55,000 dwt each committed en bloc at USD 10.5 million per unit, a 2010-built NACKS unit sold to Chinese interests at USD 14.5 million, a 2009-built Tsuneishi Zhoushan unit at USD 13.75 million, and a 2008-built Iwagi Japan unit at USD 13 million.

Handysize activity was the broadest of any size segment. A 2018-built JNS unit of 39,475 dwt committed at USD 22 million and a 2017-built JNS unit at USD 20.5 million to USD 21 million. A 2016-built Chengxi unit committed at USD 19 million, a 2015-built Jiangsu semi-boxed unit at USD 19.5 million, a 2016-built Namura Japan unit at USD 18.5 million, a 2015-built Shin Kochi logger/semi-boxed unit at USD 16.7 million, a 2014-built Korean unit acquired by Greek interests at USD 15.8 million, a 2013-built Chengxi unit at USD 16 to 17 million, and a 2009-built Japanese unit sold to Turkish interests at USD 8.6 million. Union Maritime placed a newbuilding order for two plus two Capesize vessels of 215,000 dwt at Wuhu, China, for 2028 delivery at USD 75.5 million each.

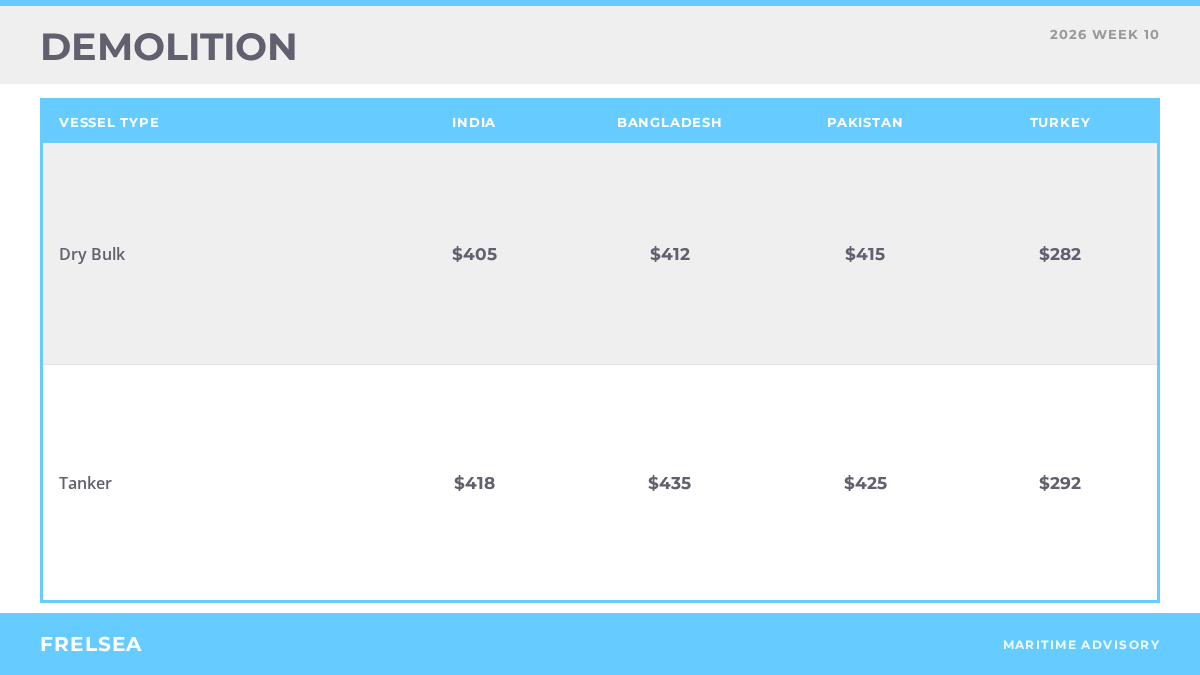

Demolition pricing was stable in Week 10 with no significant movement from the prior week in any sub-continent market. Bulker rates were indicated at USD 390 to 395 per light displacement tonne in India, USD 400 to 410 per ldt in Bangladesh, and USD 405 to 410 per ldt in Pakistan. Turkey quoted USD 270 per ldt for dry tonnage. Tanker demolition continued to command a premium across all destinations: India at USD 410 per ldt, Bangladesh at USD 430 to 435 per ldt, Pakistan at USD 415 to 430 per ldt, and Turkey at USD 280 per ldt.

Reported sales included general cargo vessels and Ro-Ro tonnage sent to India, Pakistan, and Turkey, along with a 37,320 dwt, 2003-built Korean tanker committed to Indian breakers. Transaction volumes remained modest relative to the size of the operating fleet, with owners of commercially active tonnage in both wet and dry segments retaining vessels given current secondhand price levels.