The secondhand market accelerated through early February, with dry bulk activity outpacing the prior year by a substantial margin, while tanker transactions continued at firm levels supported by steady inquiry and tight vessel availability. Across all segments, buyers demonstrated confidence in forward earnings streams, committing capital to tonnage at elevated valuations and evidence of structural demand for replacement economics.

The tanker secondhand market showed resilience amid persistent support from freight levels and narrow tonnage lists. A notable transaction occurred on the crude tanker side, with Singapore Spirit, a 318,473 DWT vessel built in 2013, changing hands to Sinokor at USD 84.5 million. This fixture underscores continued buyer confidence in modern VLCC tonnage despite elevated asset prices. The week saw VLCCs command particularly strong inquiry, with ship owners displaying bullish sentiment on forward dates and maintaining firm expectations. Suezmax activity remained steady throughout the week, supported by tight lists and consistent inquiry across regions, with TD20 rates climbing to approach 165 worldscale at week’s end. Atlantic sentiment benefited from spillover support from the VLCC market, lifting USG Suezmax rates to around 140 worldscale. The Aframax market saw measured activity with some volatility tied to cargo patterns and ballaster flows, though owners managed to hold rates firm on prompt tonnage. Mediterranean Aframaxes experienced early week strength with multiple cargoes available, though subsequent slack activity and weather deferrals dampened momentum. Product tankers continued to face structural headwinds, particularly in the Light Range segment, where overcapacity persisted and charterers aggressively pushed for lower rates. The AG LR2 segment remained particularly challenged, with ample tonnage at the disposal of charterers and rates moving either sideways or down despite some owners displaying confidence in medium-term fundamentals. The week highlighted a clear divide between crude carriers, which benefited from strong inquiry and tight tonnage lists, and product vessels, which struggled with slack demand and abundant availability.

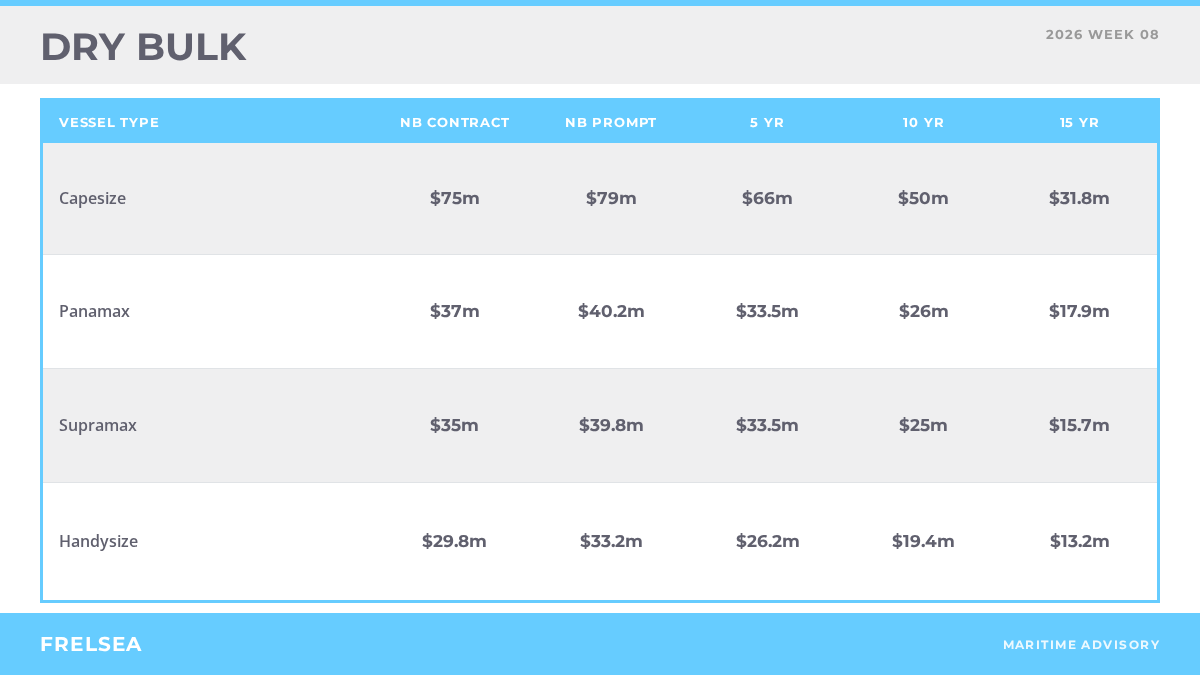

The dry bulk secondhand market displayed notable strength through the first three weeks of February, with transaction volumes outpacing the comparable 2025 period by a material margin. Shipbrokers reported 109 bulker sales across the first seven weeks of 2026, compared to 80 in the same window of 2025, representing a 36 percent year-on-year increase. Activity proved broad-based across size segments rather than concentrated in any single niche. Supramax and Handysize vessels led deal flow with 23 transactions each, followed by Ultramax at 19, Capesize at 16, and Kamsarmax at 15. The breadth of participation underscores a clearing of core working tonnage rather than speculative buying in any single segment.

The age composition shifted markedly toward mid-life tonnage, reflecting changing buyer priorities. Vessels aged 11 to 15 years accounted for 41 percent of sales, while 16 to 20 year old units represented 28 percent of activity. Vessels older than 21 years comprised only 9 percent of transactions, a sharp contraction from the prior year when older tonnage represented nearly a quarter of deal flow. This shift indicates buyer focus on remaining economic life and cargo-earning potential rather than near-term demolition optionality. Geographic supply patterns also rotated, with Chinese-built bulkers leading 2026 sales at 52 units, ahead of 37 Japanese-built and 13 Korean-built vessels. This represents a reversal from the prior year period, when Japanese-built tonnage dominated, reflecting gradual re-rating of Chinese-built vessel quality and attractiveness in mid-size segments.

Notable Capesize transactions included Cape Brazil, a 177,897 DWT unit built in 2010, sold at USD 31 million, a gain of approximately USD 7.75 million on the EUR 23.25 million achieved on similar tonnage six months prior. Explorer America, an Ultramax of 61,000 DWT, was fixed at USD 18.2 million to Chinese interests, while the one-year-younger sister vessel achieved USD 19.2 million, indicating modest appreciation in mid-life tonnage. The Nord Chesapeake, a modern 60,000 DWT Kamsarmax fitted with scrubber equipment, commanded USD 25.5 million. On the Supramax segment, Fortune Tiger, a 58,000 DWT unit built in 2013, was committed at USD 19 million. Handysize vessels showed consistent activity, with Liberator, a 28,000 DWT unit, matching prior week pricing at USD 6.7 million. These transactions occurred against a backdrop of firm asset valuations, with five year highs posted across most benchmark segments, yet buyer appetite remained intact. One-year asset appreciation reached 22 percent for ten year old Capesizes, 10 percent for Kamsarmaxes, and 18 to 19 percent for mid-size tonnage. This sustained buyer activity at elevated prices signals underlying confidence in forward cash generation despite challenging financing economics.

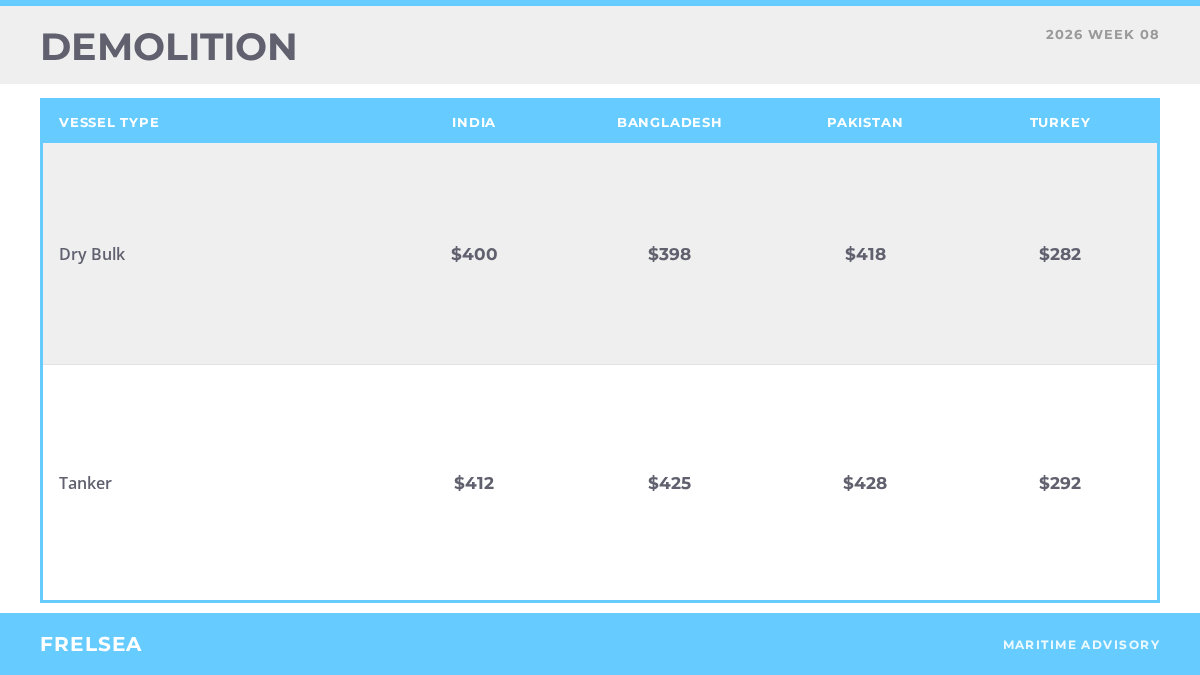

No demolition transactions were reported during this reporting week.

Market Snapshot

The secondhand market continues to process increased offer flow while prices remain elevated by historical standards. The breadth of participation across vessel sizes suggests an underlying confidence in operational cash flows, offsetting financing costs and moderating ordering appetite for newbuilding tonnage. Tight tonnage lists and period strength in core freight routes are expected to support ongoing secondhand activity in coming weeks.