The secondhand market in Week 7 reflected strengthening fundamentals across both tanker and dry bulk sectors, with freight momentum driving asset prices to cycle highs and limited modern tonnage availability intensifying competition for eco-efficient vessels.

The tanker secondhand market remained resilient through Week 7, supported by steady freight undertones and sustained owner confidence despite seasonal post-Chinese New Year softness. VLCC values held firm at USD 86.5–89 million, with Sinokor acquiring the scrubber-fitted sisters “Ilma” and “Ingrid” at USD 89 million each and the “Eagle Varna” at USD 86.5 million, signalling strong Asian operator interest in modern crude tonnage. Suezmaxes showed notable appreciation, with modern 2022-built sisters “Emeraldway” and “Sunriseway” trading to Greek interests at USD 88 million each, while the CAP1 unit “Nordic Pollux” transacted at USD 25 million, indicating valuation support across vintage segments.

Aframax and LR2 valuations showed firm momentum, with coated and scrubber-fitted sisters “FS Diligence” and “FS Endeavor” selling to Greek buyers at USD 86 million each, while LR1 units traded enbloc and individually near USD 15–42 million. Product tanker activity remained steady, with MR tonnage including the ice-class sisters “Elandra Fjord” and “Elandra Baltic” trading at USD 24.5 million each. Scrubber-fitted units commanded sustained premiums, supported by strong charterer demand for fuel-efficient tonnage with extended operational horizons. LR and MR vessel demand remained underpinned by regional trading opportunities, with MR2 units near USD 14 million also recording transactions.

The dry bulk secondhand market entered Week 7 on exceptionally strong footing, with Capesize values reaching their highest levels since 2008. A 16-year-old Japanese-built Capesize transacted at mid-to-high USD 32 million, implying benchmark valuations for 15-year-old units at high USD 34 million—a 19% premium to 2024 averages and the strongest level since September 2008. Since October 2025 alone, 5- and 10-year-old Capesize prices increased by approximately 6%, while 15-year-old units surged roughly 25%, with owners demonstrating clear reluctance to sell modern eco-vessels amid improving earnings visibility and strong freight momentum.

Major transactions reflected broad-based strength. The “Star Scarlett,” a 175,649-dwt 2014 Jinhai-built Capesize, traded to Chinese interests at USD 36 million, while the “Michalis H,” a 180,355-dwt 2012 Dalian-built unit, sold at USD 35.2 million with timecharter attached at USD 27,250/day through Q4 2026. The “Smyrna” and “Cape Brazil” concluded at USD 25.25 million and USD 31 million respectively, while the “Epic,” a 182,060-dwt 2010 Odense-built Capesize, sold for USD 32.2 million. In the Post Panamax segment, the “Royal Award” sold to Chinese buyers at USD 11.5 million, while “Bulk Xaymaca” transacted at USD 9.4 million. Kamsarmax values tracked Q3–Q4 2024 levels, with “Anglo Red” and “Anglo Barinthus” each at USD 17.1 million, “Gastone” at USD 17.5 million, and “Athina Carras” at USD 17.0 million. Supramax and Handysize segments remained broadly aligned with 2024 peaks at USD 7.5–19 million, including “Fortune Tiger” at USD 19 million and “Hunan” and “Powan” at USD 19 million each. Limited availability of prompt modern eco-tonnage emerged as a critical market driver, with buyers competing aggressively for fuel-efficient units, exerting sustained upward pressure on 5- and 10-year-old vessel segments.

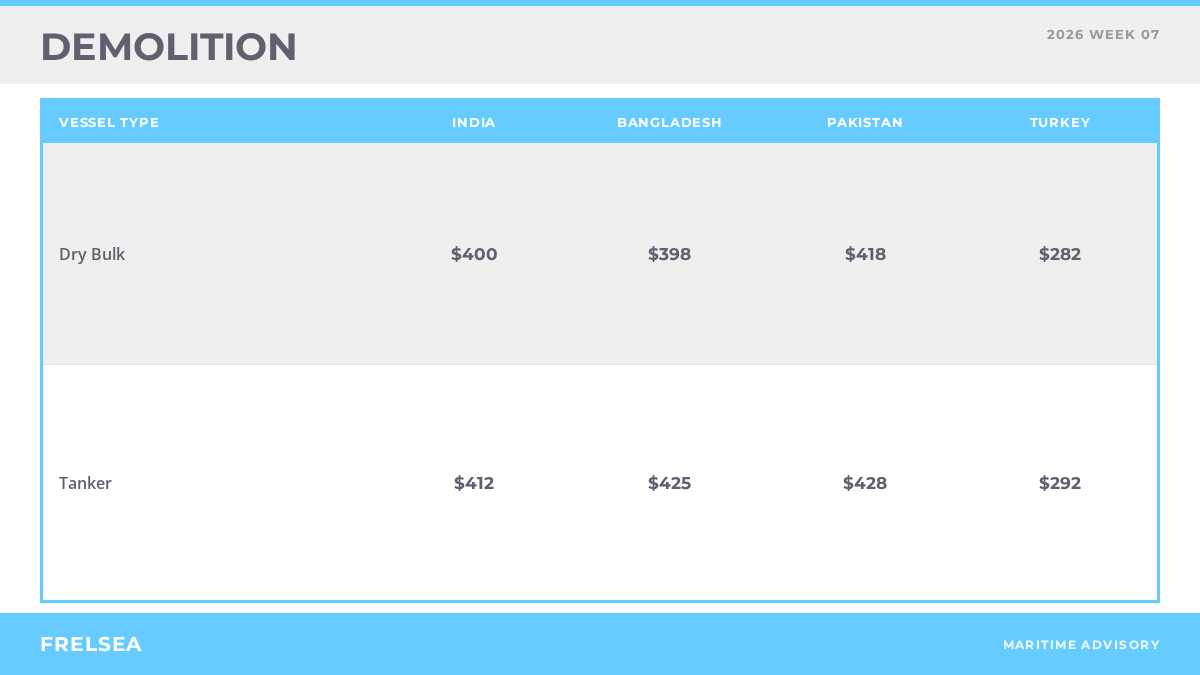

Demolition activity remained selective through Week 7, with recycling prices reflecting broader scrap steel market dynamics. Indian recyclers maintained their dominant market position, securing the majority of tonnage offered. The 28,255-dwt 1995 Japanese-built bulk carrier traded at USD 425 per lightweight tonne to Bangladesh, while the 12,352-dwt 1982 Japanese-built general cargo unit “Lily-HA” concluded with Turkey at undisclosed levels, and the 6,902-dwt 2001 Korean-built tanker “JMA” traded to India at undisclosed prices, reflecting typical pricing floors for these vessel categories.

Recycling yard pricing in the Indian market held at approximately USD 410–430 per lightweight tonne for bulk carriers, with Bangladeshi yards marginally stronger at USD 420–430 per ton and Pakistani yards at USD 430–440 per ton. Turkish outlets offered limited alternatives at substantially softer levels near USD 280–300 per ton. Activity remained constrained by limited fresh tonnage offerings as owners deferred demolition decisions amid continued freight improvements and opportunities to generate returns through extended trading or sale at cycle highs. Tanker demolition pricing showed similar strength, with Indian recyclers quoting approximately USD 450 per lightweight tonne, further supporting the broader trend of constrained demo supply driven by improved market fundamentals.