The secondhand markets remained steady through week six, with sustained interest across tanker and dry bulk sectors reflecting balanced supply-demand conditions. Newbuilding deliveries continued at elevated levels, while selective tonnage continued to find new owners at stable pricing throughout the period.

VLCC valuations held firm during the week, supported by continued acquisition activity from major charterers and operators. The scrubber-fitted “DHT Bauhinia” 301,000 dwt 2007-built committed at USD 51.5 million represented solid confidence in the modern crude carrier segment. Greek interests acquired the newer “Asian Lion” 297,000 dwt 2009-built at USD 60 million, reflecting the premium placed on more recent tonnage with extended compliance certification. Earlier comparable transactions had established the “Advantage Value” 297,000 dwt at USD 55 million, showing consistent regional and age-related pricing patterns across the VLCC market.

Mid-range activity remained brisk, with the MR2 “Seaways Grace” and “Seaways Madeleine” both 50,000 dwt 2008-built committing at USD 16 million each. This indicated sustained demand for modern medium-range vessels with standard compliance profiles. Suezmax tonnage saw continued Greek activity, with regional operators maintaining selective purchase programs for both scrubber-fitted and conventional units across multiple yard origins.

Newbuilding orders in the tanker sector reflected the broader trend toward replacement-driven delivery schedules. Major orders were placed with Chinese and Korean yards, with delivery windows predominantly 2028-2029. Scrubber-fitted specifications and LNG-ready features appeared standard on larger orders, indicating the industry’s continued commitment to environmental and fuel flexibility requirements. The overall activity pattern suggested that fleet growth remains disciplined, with incoming tonnage largely offset by aging vessel retirements rather than adding net capacity.

Capesize activity in the sales and purchase market continued at measured pace. The 180,000 dwt “Irene II” 2006-built committed to Chinese interests at USD 21 million represented solid pricing for the segment, while earlier comparable vessels like the 180,000 dwt “Montecristo” 2005-built had traded at USD 20 million. This pricing alignment suggests consistent valuation across similar tonnage and ages. The 174,000 dwt “Robusto” 2006-built committed at USD 19.5 million on a Q2 2026 delivery basis, with the comparable sister “Pompano” having been placed at USD 17 million in December, showing the impact of delivery timing on valuation.

Kamsarmax and Panamax tonnage remained the most active segments. The kamsarmax “Athina Carras” 82,000 dwt 2012-built sold to Greek interests at USD 17.5 million, with the closely-comparable “Rize” 82,000 dwt same year and builder unit also committing at USD 17.6 million. Prior year comparables indicated pricing has held stable, as the one-year-older “Montana I” 82,000 dwt had traded at USD 15.4 million in October. Panamax tonnage showed continued Chinese buyer interest, particularly for conventional units suitable for regional trading patterns.

Ultramax and supramax vessels saw steady engagement, with the 63,000 dwt “Mitsos” 2013-built committing at USD 20.5 million, attracting Greek ownership. The segment benefited from persistent cargo availability across multiple trades and continued employment opportunities for modern tonnage. Handysize vessels maintained interest levels consistent with earlier weeks, with units ranging from 28,000 to 36,000 dwt finding buyers at prices reflecting their age and builder credentials.

Newbuilding commitments across dry bulk remained focused on replacement-driven schedules through 2028, with Chinese and Korean yards receiving orders predominantly in the 82,000 to 205,000 dwt categories. Delivery dates clustered around 2027-2029, suggesting orderbook maturity in coming years. Activity levels indicate that fleet growth remains constrained by balanced newbuilding discipline and continued reliance on older tonnage for marginal capacity.

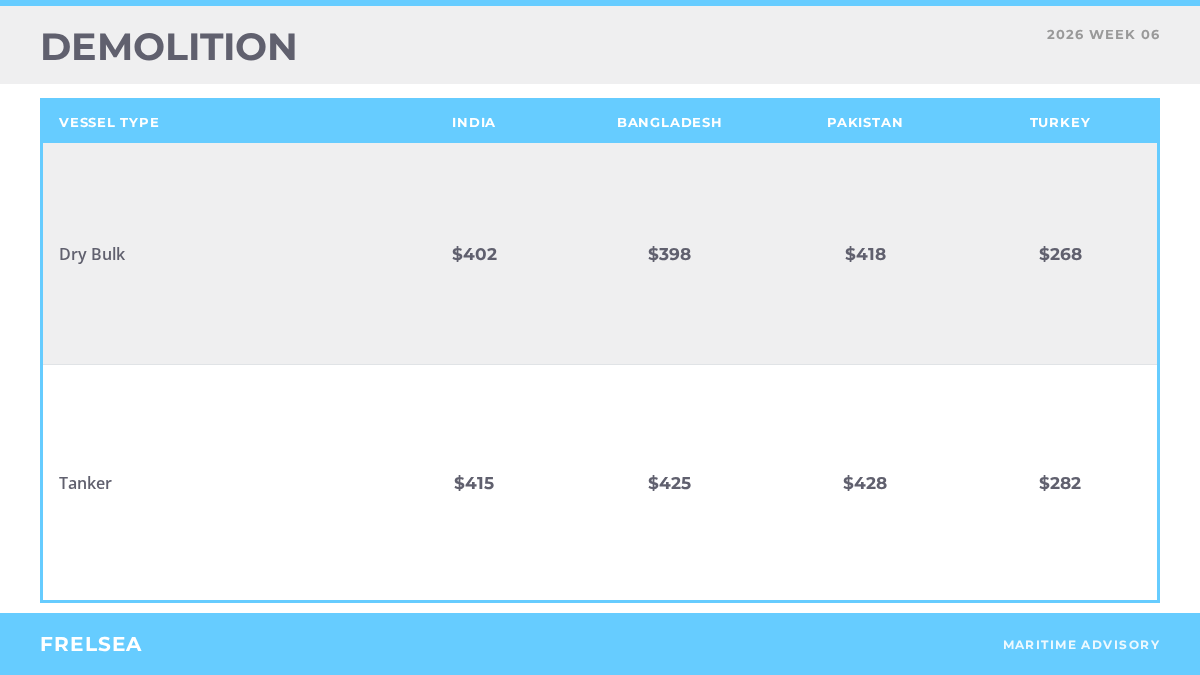

Demolition activity remained selective during the week, with scrapping decisions continuing to reflect current market valuations and age profiles. While headline data on demolition tonnage was limited, the broader fleet age analysis suggests that demolition rates will depend less on current valuations than on future scrapping momentum through 2026-2028. Replacement ratios in MR2, Aframax and Suezmax segments indicate incoming tonnage broadly matches or exceeds aging 21-year-old cohorts, pointing to a structurally balanced approach to fleet management rather than aggressive retirements.

The limited availability of tonnage suitable for immediate scrapping continues, with most available older vessels still generating adequate employment returns under current freight regimes. Only the oldest conventional units without modern compliance features or extensive renovation records appeared to approach breaking thresholds. Regional demolition capacity in South Asia remains constrained, with limited availability for immediate recycling across primary breaker locations.