Secondhand tanker values surged to multi-year highs in Week 05 as geopolitical drivers and extended trade routes locked in earnings momentum, while dry bulk S&P activity exploded to a five-year peak despite already elevated price levels.

The tanker secondhand market experienced remarkable momentum, with Very Large Crude Carriers commanding record valuations. A 300,000 dwt VLCC sold at USD 90 million, while a 299,991 dwt unit from 2013 achieved low USD 90s. A 298,000 dwt 2009-built Suezmax came away at USD 60 million, reflecting persistent strength in crude segment valuations. In the Aframax sector, two 109,999 dwt newbuild-equivalent tankers from 2023-24 traded at USD 84 million each, while a 2009-built 107,605 dwt Aframax sold at USD 35.5 million. LR1 deals showed USD 11.3 million for a 70,558 dwt 2005-built, and MR2 trading included a 53,688 dwt 2006-built at USD 13.0 million and a 50,844 dwt 2014-built at USD 31.0 million. Smaller product tankers also moved, with a 46,843 dwt MR from 2005 achieving USD 9.7 million. The week’s activity underscores how sanctions-driven longer routings and transition-linked scrubber investments continue to elevate acceptable asking prices across the crude and product tanker spectrum.

Newbuilding orders for tankers reflected brisk pace heading into February, with multiple VLCC and Suezmax contracts placed at Chinese yards. Hengli secured orders for 6+4 units of 306,000 dwt VLCC at USD 120 million each with scrubber equipment and H2 2028 delivery windows. New Times added 2 units of 302,000 dwt tankers at USD 118 million with 2029 options. Suezmax contracting was similarly active, with Daehan securing 2 units at USD 86 million each for Q3 2028 delivery and another pair at USD 85 million with scrubber fit for Q2 2029. Hyundai Samho recorded 2 units of 158,000 dwt at USD 87 million each for H1 2029, confirming that owners remain committed to locked-in newbuild tonnage despite already-elevated secondhand levels. Smaller tankers moved as well, with 2 units of 50,000 dwt ordered at Guangzhou Shipyard at USD 52 million each for 2028 delivery.

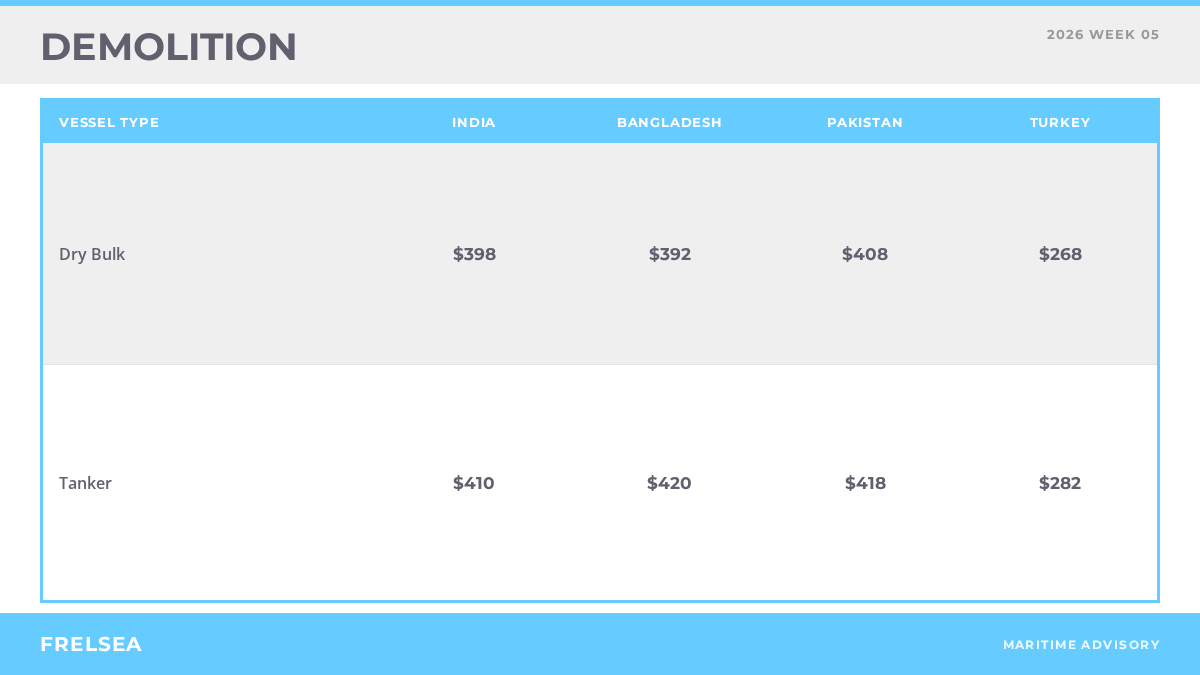

Demolition values remained steady across South Asia, with tankers commanding premium pricing. India held at USD 410 per light displacement tonne, Bangladesh at USD 430, and Pakistan at USD 420. A handful of tonnage found its way to recycling yards, including a 106,547 dwt tanker from 1997 at India for USD 357 per ldt and a 46,166 dwt tanker from 1996 at Singapore for USD 435 per ldt as-is. Turkish recyclers operated at USD 280 per ldt, remaining structurally lower than subcontinent yards.

The dry bulk secondhand market posted record transaction volumes for January, with 71 bulkers sold versus 52 in the prior-year month. Capesize transactions dominated headline sales, with a 185,897 dwt 2005-built achieving USD 18.5 million and a 177,173 dwt 2005-built at undisclosed levels near market. Kamsarmax trading included an 82,992 dwt 2006-built at USD 10.7 million and an 81,950 dwt 2012-built at USD 17.7 million to Greek buyers. Panamax activity showed a 75,484 dwt 1999-built at USD 6.1 million to Chinese buyers, a 74,916 dwt 2011-built at USD 15.3 million, and a 74,886 dwt 2011-built at USD 16.7 million to Greek interests. Supramax proved the headline sector, with 27 sales recorded across the month. A 58,052 dwt 2014-built achieved USD 21.5 million to Greek interests, while other Supramax tonnage filled the mid-USD 10–13 million range. Handysize units remained active with a 33,774 dwt 2011-built achieving USD 11.0 million.

Newbuilding orders for dry bulk reflected robust demand despite already-elevated secondhand values. Capesize activity included 2 units of 210,000 dwt at DACKS, China for 2029 delivery with scrubber fit at undisclosed pricing, and 2 units of 82,500 dwt at Cosco Yangzhou for 2028-29 delivery at undisclosed levels. Seacon Shipping Group secured 6 units of 63,800 dwt Ultramax newbuilds at Qidong Xiangyu for 2027 delivery at USD 32.8 million each. The sustained clip of newbuild fixing underscores owner comfort with locking in ton-mile optionality despite the combined headwind of elevated secondhand and constrained delivery slots.

Demolition pricing for dry bulk remained firmly anchored in South Asia. India held at USD 390 per ldt, Bangladesh at USD 380, and Pakistan at USD 400. Turkish yards operated at USD 270 per ldt. A limited number of bulkers reached the breakers, including a 28,510 dwt 1994-built at India for USD 405 per ldt.

Demolition markets across South Asia and Turkey maintained structural stability as the month closed. Tankers outpriced bulkers across all major recycling centers, reflecting differential scrap composition and steel quality. Subcontinent markets held firmer than Turkish alternatives, with India and Bangladesh each USD 60–70 per ldt higher than Aliaga. No significant demolition tonnage emerged in the reported sales for the week, though market tone remained constructive ahead of the February tidal windows at Chattogram and Alang.