Week 04 demonstrated measured activity across both tanker and dry bulk secondhand and newbuilding markets, with demolition demand providing steady support for older vessels across multiple Asian recycling centers. Transaction volumes remained consistent with historical patterns for the period, reflecting equilibrium between buyer interest and available tonnage.

Tanker secondhand sales continued to register across multiple size classes with stable pricing in the modern segment. A Newcastlemax achieved USD 74 million to Korean interests, consistent with comparable modern vessels sold in preceding weeks at USD 73.6 million. This price range reflects buyer confidence in supertanker values despite broader market uncertainties. An Aframax traded at USD 35.5 million to Chinese interests, maintaining parity with similar vessel sales from earlier in the quarter, indicating sustained demand for mid-sized crude carriers. LR1 sales registered at USD 10.2 million and USD 13.5 million, reflecting the typical variance in pricing based on vessel age and condition differences. MR product tankers showed a broader range with sales recorded between USD 10 million and USD 31 million, demonstrating varied buyer interest across the product tanker segment. A chemical tanker transaction occurred at USD 14 million, adding to the overall breadth of market activity. Newbuilding enquiry remained consistently active with major builder engagement. VLCC newbuilding commitments proceeded for Greek owners at USD 120 million per unit for 306,000 dwt vessels, while LR2 newbuildings attracted orders at USD 86 million per unit for 157,000 dwt specifications. Smaller product tankers, particularly 50,000 dwt MR units, generated ongoing buyer interest across Chinese shipyard capacity, reflecting the market’s continued appetite for economical product carrier newbuilding tonnage at competitive pricing levels.

The dry bulk secondhand market recorded broad transactional activity across all major size categories. Capesize sales remained range-bound between USD 31.5 million and USD 32 million for mid-age tonnage built in 2011 and 2012, demonstrating sustained buyer appetite for vessels in the five to thirteen-year age bracket. This price consistency suggests stable expectations for secondhand Capesize fundamentals. Kamsarmax vessels transacted across a wider spread, with pricing between USD 16.8 million and USD 20 million for units primarily in the older segment, reflecting age-related differentiation in the handy-sized bulker category. Panamax tonnage moved at USD 16 million, contributing to healthy transaction volume across size classes. Ultramax sales showed notable diversity in values correlated with modern specifications and equipment. A modern 2020-built Ultramax traded at USD 30 million, while a 2025-built unit with scrubber capability achieved USD 34 million, reflecting the enhanced value placed on newer tonnage with environmental compliance features. Older Ultramax units sold at lower levels commensurate with their age and specification disadvantages. Handysize vessels demonstrated consistent market activity with 2012-built units achieving USD 10 million and older tonnage selling across the USD 4 million to USD 11.4 million range. This breadth of transactions at various price points underscores steady demand for smaller bulkers across multiple buyer segments. Newbuilding commitments continued to favor Japanese yards for modern Capesize specifications, with contracts proceeding at undisclosed pricing. Smaller Capesize newbuilding orders persisted with Chinese shipyard activity at comparable levels to prior weeks, maintaining the established pattern of regional builder competition for newbuilding tonnage in the modern Capesize category.

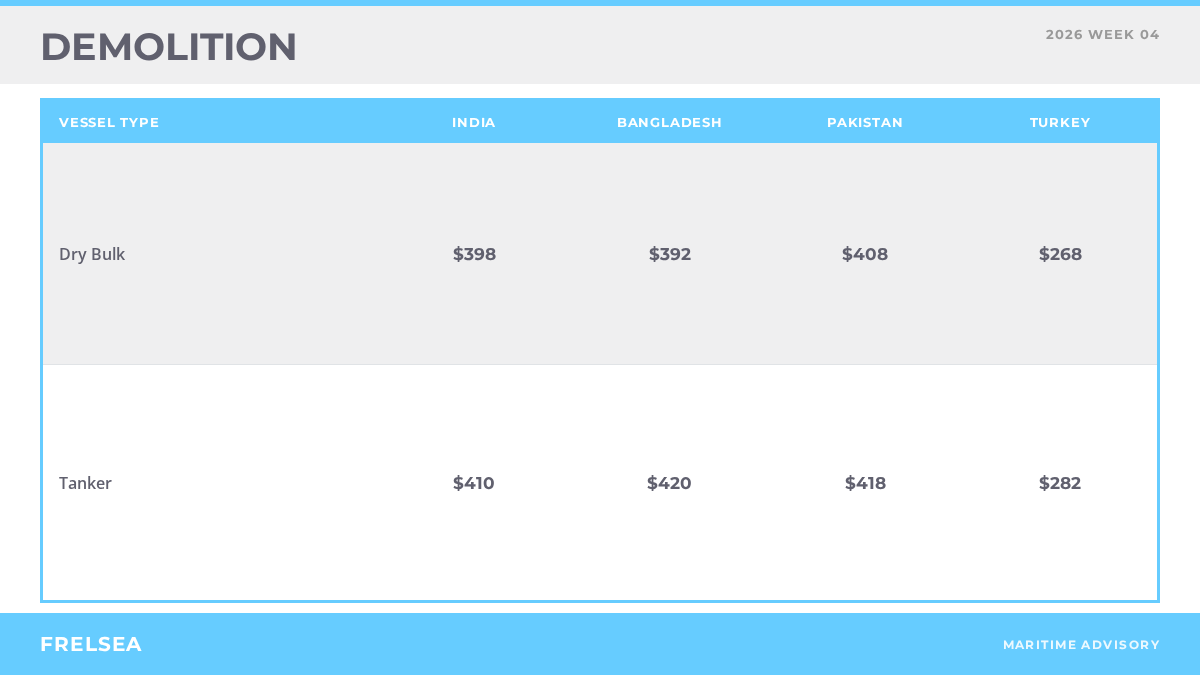

Demolition markets retained steady support across Asian recycling centers, with regional variations reflecting local supply conditions and recycler appetites. Pakistan maintained firm pricing at USD 412 per light displacement tonne, demonstrating strong recycler demand for inbound tonnage. Bangladesh and India remained competitive at USD 398 and USD 412 per light displacement tonne respectively for transacted tonnage, though both markets showed capability to adjust pricing based on supply flow. Turkey continued to offer lower pricing at USD 270-280 per light displacement tonne, reflecting lower local operating costs and alternative market dynamics. Indicative pricing guidance across major yards reflected modest softness in some segments while maintaining floor support. India quoted steady pricing at USD 390 per light displacement tonne for bulker tonnage and USD 405 for tanker tonnage, reflecting the traditional premium for tanker recycling value. Bangladesh indicated pricing at USD 380 per light displacement tonne for bulkers and USD 415 for tankers, maintaining spread differentials aligned with market convention. Pakistan’s firm quotations of USD 400 for bulkers and USD 410 for tankers demonstrated the market’s strength in that region. A bulker yard in Oman accepted tonnage at USD 398 per light displacement tonne, indicating both the geographic reach of recycling demand beyond the primary South Asian centers and the willingness of alternative locations to participate in market pricing. The range of pricing across geographies reflects variation in recycler efficiency, local cost structures, and the competitive dynamics driving older tonnage allocation decisions in the global vessel recycling sector.