Tanker sales accelerated in week 3, with major portfolio acquisitions alongside individual vessel transactions, while dry bulk activity broadened across all sizes and newbuilding orders continued at established price levels.

VLCC transactions dominated the week’s secondhand market, reflecting consolidation activity and strategic acquisitions. Sinokor Maritime executed a significant portfolio acquisition of approximately 30 vessels during the Christmas period, with several large modern units changing hands at firm prices. Trafigura acquired three modern VLCCs enbloc, securing the 313,000 dwt “Spherical” (2022, Imabari) for USD 130 million, and two sister vessels “Hunter” and “Serendipity” (both 2021, Hyundai Samho) for USD 250 million combined. Additional modern VLCC sales included the 319,911 dwt “Delta Angelica” (2012, Hyundai) and the similarly-sized “Delta Glory” (2012, Hyundai), both trading at USD 80 million. The 321,300 dwt “Atlantas” (2010, Daewoo) commanded USD 140 million from Korean interests on a multi-vessel basis, while a suite of Front-series VLCCs transitioned to Korean ownership for USD 831.5 million enbloc.

LR3 and LR2 trading showed softer valuations. The 158,933 dwt “Eclipse I” (2006, Hyundai Samho) committed at USD 33 million, with comparable 2006-2007 built units trading in the USD 33 to USD 35 million range. The 109,999 dwt “STI Kingsway” (2015, Sungdong) achieved USD 57.5 million on scrubber-fitted specifications. Mid-range product tanker (MR) activity showed continued interest in modern tonnage, with the 49,999 dwt “Tranquility” (2020, Guangzhou) sold at USD 39 million, and the 46,784 dwt “Ellie M II” (2007, Hyundai Mipo) trading at USD 15 million.

Newbuilding commitments for tankers included VLCC orders at established price points. Japanese buyers placed a 310,000 dwt VLCC with JMU for 2029 delivery, while Norwegian ownership secured two 306,000 dwt units from Hengli for 2028 delivery. Omani interests contracted three 300,000 dwt VLCCs from Hanwha Ocean for 2028-2029 delivery at USD 129.5 million per unit on scrubber-fitted, dual-fuel ready basis. Smaller newbuilding orders included two 157,000 dwt LR2 tankers from DH Shipbuilding, with Greek buyers committed at USD 85 to USD 86 million each.

Dry bulk secondhand activity spanned all major classes, supported by persistent, if cautious, buyer interest. In the capesize sector, the 181,408 dwt “Mineral Honshu” (2012, Koyo) sold to Chinese interests for USD 37.7 million, with the sistership “KM Osaka” (180,652 dwt, 2012, Koyo) executing at USD 34.8 million. These units established a market level around USD 34 to USD 38 million for modern 2012-built capesize tonnage. The 209,523 dwt “Nord Palladium” (2021, SWS) commanded USD 76.25 million from Chinese ownership, roughly USD 2.5 million above comparable 2020-built newcastlemax pricing a month prior, signaling modest premium appreciation on 2021 construction.

Kamsarmax and panamax sales remained active. The 81,810 dwt “BW Matsuyama” (2019, Tsuneishi Cebu) sold to Greek interests for USD 31 million, while the 82,158 dwt “Magic Perseus” (2013, Tsuneishi) transacted as a sale-and-leaseback arrangement at USD 15.6 million. Older kamsarmax tonnage, including the 80,323 dwt “Jag Aarati” (2011, STX), committed at USD 14 million, reflecting typical 2011-built valuations in the mid-USD 14 to USD 15 million band.

Ultramax and supramax tonnage showed consistent turnover across all ages. The modern 61,222 dwt “Starry Night” (2022, NACKS China) achieved USD 32.5 million to Greek ownership, whilst the 61,360 dwt “Explorer Africa” (2012, Oshima) traded at USD 19.2 million. Supramax units ranged broadly: the 57,412 dwt “Desert Glory” (2011, Hyundai Mipo) commanded high USD 14 million, and the 56,898 dwt “Pisti” (2011, Cosco) sold at USD 12.8 million, establishing typical pricing for 2011 supramax tonnage around USD 12.8 to USD 15 million. Handysize activity included the 36,699 dwt “TBC Praise” (2012, Hyundai Mipo) at USD 14.4 million and the older 33,520 dwt “Bass Strait” (2006, Hakodate) at USD 8.6 million.

Newbuilding orders in dry bulk consisted primarily of larger tonnage. Two 210,000 dwt units from Qingdao Beihai committed to Chinese ownership at USD 75 million per unit on methanol and ammonia-ready, scrubber-fitted specifications. Three additional 210,000 dwt newcastlemax units from the same yard proceeded on firm contract with Cosco Shipping. Smaller orders included two supramaxes plus two options (63,500 dwt, Jiangsu Soho Chuangke) valued at USD 33.4 million for the fixed tranche, destined for Chinese ownership.

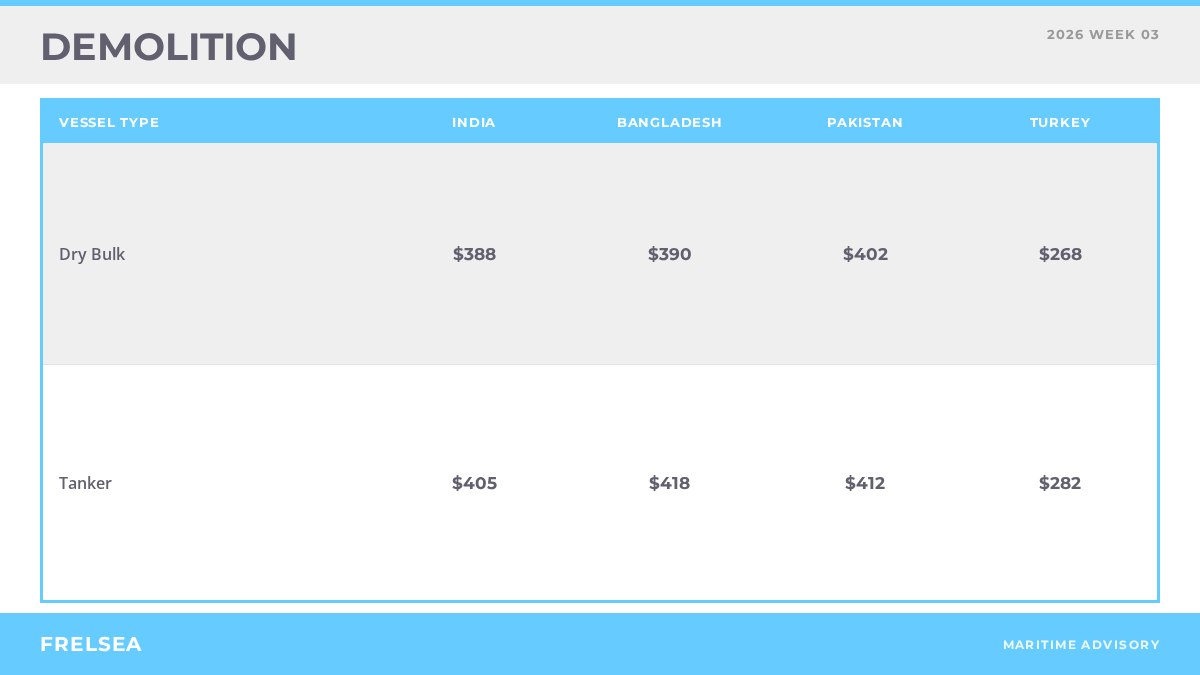

Demolition prices remained stable across South Asian breaking yards with only limited activity reported. India maintained indicative levels of USD 390 per ldt for bulker demolition and USD 405 per ldt for tankers. Bangladesh prices stood at USD 375 per ldt bulkers and USD 410 per ldt tankers, whilst Pakistan quoted USD 400 per ldt bulkers and USD 410 per ldt tankers. Turkish demolition yards remained at a significant discount, quoting USD 270 per ldt across both bulker and tanker segments. Reported sales were sparse: the 28,510 dwt “Sheng Lu” (1994 bulker) and the 13,770 dwt “Dimple” (1992 bulker) completed, with the latter achieving USD 388 per ldt in India, indicating modest pricing within the stated indicative range.