The opening week of 2026 delivered mixed momentum across secondhand markets, with tanker activity dominated by large enbloc deals while dry bulk showed selective transactional activity across multiple size segments. Geopolitical shifts in Venezuela sparked renewed interest in compliant mainstream tonnage, particularly Aframaxes and Suezmaxes positioned for legitimate crude flows.

The VLCC market remained the principal focus for secondhand tonnage activity. A sizeable enbloc transaction dominated the segment, involving eight South Korean VLCCs built in 2015 and 2016, all circa 300,000 dwt, sold to an undisclosed buyer for a combined USD 831.5 million, averaging USD 104 million per vessel. These vessels, constructed at Daewoo and Hyundai Samho yards, reflected current resale valuations across the modern fleet. Separately, Sinokor emerged as an active buyer, acquiring the scrubber-fitted OCEANIS at 321,000 dwt (2011 Samsung) for USD 68 million. The same buyer also secured the modern DESIMI and SOLANA, both circa 297,000 dwt (2011 Shanghai Jiangnan), sold enbloc for USD 136 million. A further enbloc transaction saw the scrubber-fitted ATLANTAS at 321,300 dwt (2010 Daewoo) and ACHILLEAS at 298,000 dwt (2010 Universal Ariake) sold together for USD 140 million. Sinokor was also linked to acquisition of ADVANTAGE VALUE at 298,000 dwt (2009 Shanghai Jiangnan) for USD 55 million, signaling sustained appetite for compliant modern tonnage.

The Suezmax segment saw lighter but steady activity. ECLIPSE I at 159,000 dwt (2006 Hyundai Samho) traded at USD 33 million, while NORDIC LUNA at 150,000 dwt (2004 Universal Tsu) sold for USD 25 million. NORDIC SPRINTER at 159,000 dwt (2005 HHI) changed hands for USD 25 million. In the smaller product tanker space, the coated LR2 PELAGIC TOPE at 77,000 dwt (2008 Dalian) fetched USD 13.8 million. The LR2 segment also saw STI Kingsway at 110,000 dwt (2015 Sungdong), scrubber-fitted, trade for USD 57.5 million, reflecting strong valuations for modern eco-compliant tonnage. Greek buyers acquired two modern zinc-coated MR2s, MARITIME TRANQUILITY and MARITIME COMITY, both 50,000 dwt (2020 GSI), for USD 39 million each. Additionally, a CMB.Tech portfolio sale involved six VLCCs at a combined USD 261.1 million.

Capesize activity showed limited but quality-focused transactions. NORD PALLADIUM at 210,000 dwt (2021 SWS) sold to Zhejiang Shipping for USD 76.25 million, representing strong modern tonnage valuations. In the traditional capesize segment, KM OSAKA at 181,000 dwt (2012 Koyo) was sold to Chinese buyers for USD 34.8 million. GOLDEN MAGNUM at 179,788 dwt (2009 Daewoo), fitted with scrubber, traded at USD 28.7 million, while its sister vessel EUROPE at 179,448 dwt (2010 Daewoo) sold for USD 30.9 million. These transactions reflected the differential between modern eco-compliant tonnage and conventional vessel pricing.

Kamsarmax activity dominated mid-size bulk trades. BW MATSUYAMA at 82,000 dwt (2019 Tsuneishi Cebu) changed hands for USD 31 million to undisclosed interests. CENTURY SHANGHAI at 82,000 dwt (2018 Chengxi) sold via online auction for USD 25.02 million, suggesting price discovery through competitive bidding mechanisms. SEACON SHANGHAI at 80,811 dwt (2019 Wenchong) was sold to Dexter Navigation for USD 26.7 million. Smaller kamsarmax activity included JAG AARATI at 80,323 dwt (2011 STX) trading for USD 14.75 million, demonstrating sustained demand across the panamax-kamsarmax band.

The Ultramax sector reflected steady owner and charterer interest. STARRY NIGHT at 61,000 dwt (2022 NACKS) sold for USD 32.5 million, commanding premium pricing for ultra-modern tonnage. OCEAN JASMIN at 63,465 dwt (2019 COSCO Qidong) traded for USD 28.5 million with an attached time charter through June 2026 at maximum. EXPLORER AFRICA at 62,000 dwt (2012 Oshima) changed hands for approximately USD 19 million.

Supramax transactional activity remained modest. DESERT GLORY at 57,412 dwt (2011 HMD) sold to European buyers for approximately USD 14 million. SUN MASTER at 50,714 dwt (2011 Oshima) was acquired by Greek interests for approximately USD 15 million, with OHBS status and survey due noted. These sales indicated continued interest in modernizing Greek and European owned fleets.

Handysize activity remained constrained. BULKER BEE 30 at 34,904 dwt (2010 TK Shipbuilding) traded for USD 11.3 million. BASS STRAIT at 33,520 dwt (2006 Hakodate) sold to Fu Yuan Marine for USD 8.6 million. In smaller segments, JIANG YUAN NAN JING at 49,326 dwt (2003 NACKS) sold via auction for USD 7.5 million, while TBC PRAISE at 36,699 dwt (2012 Hyundai Mipo) also transacted, reflecting selective buying on more competitively priced tonnage.

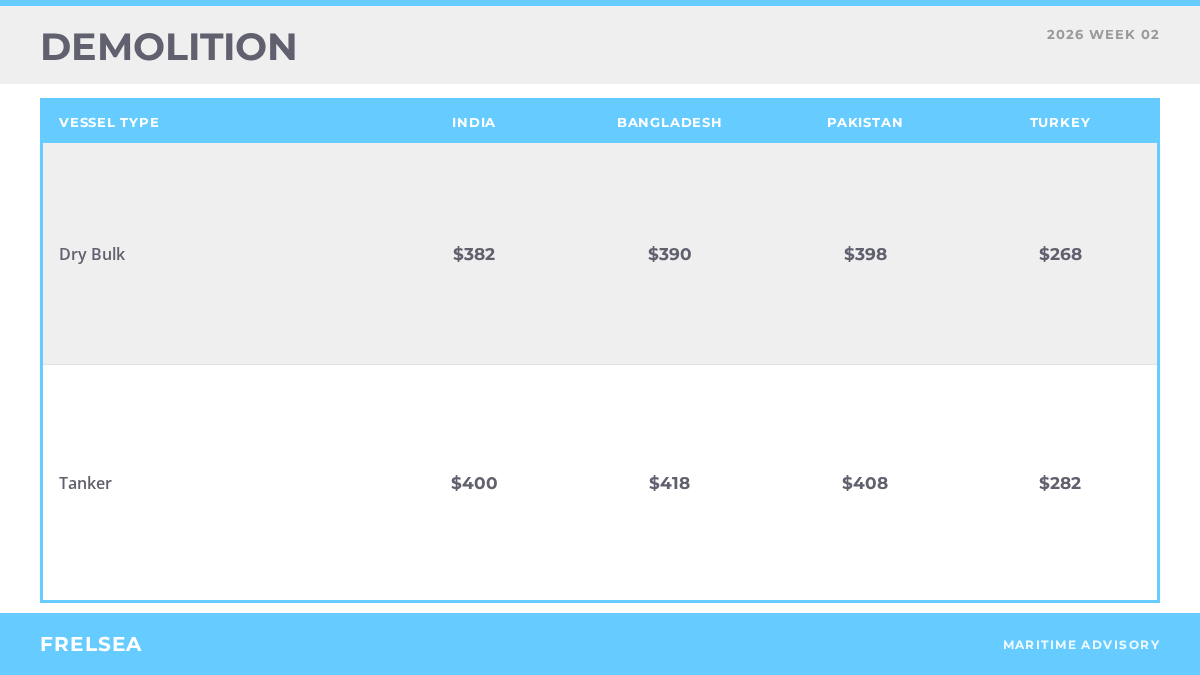

Demolition activity remained subdued during the week with limited reportage. SEPETIBA BAY at 35,036 dwt (2012 Samjin) was reported sold for breaking at USD 11 million, representing typical residual value recovery within current market parameters. Scrap steel price dynamics and recycling yard capacity utilization continued to reflect post-holiday seasonal adjustment patterns across primary breaking locations in India and Bangladesh. The absence of sustained tonnage flow to demolition, particularly in the bulker segment, suggested that most aging vessels found alternative employment routes rather than immediate scrapping. Market participants observed that geopolitical factors, particularly the Venezuelan crude flow reorientation, created incremental demand for compliant mainstream tonnage, effectively absorbing potential demolition candidates into secondary market channels. Activity in this sector is expected to resume more normalcy following Chinese New Year holidays and once the broader impact of Venezuelan market restructuring becomes clearer.